The numbers are no longer speculative. Coherent Market Insights values the global humanoid robot market at USD 6.40 billion in 2026, growing at a 49.0% CAGR to USD 104.95 billion by 2033. Within that figure, Asia-Pacific stands out as the single fastest-growing region — Grand View Research sizes APAC humanoid revenue at approximately USD 478 million in 2026 and projects growth to USD 922 million by 2030 at a 17.9% CAGR.

Mordor Intelligence's estimate is more aggressive: Asia-Pacific on a 53.2% CAGR — the steepest of any geography globally. The variation between forecasters reflects genuine methodological differences in how they segment industrial, service, and research robots. But the directional consensus is unambiguous: APAC leads, and the lead is widening.

Three Forces Driving APAC's Outperformance

Every major forecaster cites the same structural drivers behind APAC's premium growth rate. First, China's manufacturing base — the world's largest by output — creates an unmatched home market for industrial humanoid deployment. Factory operators who have already automated repetitive tasks with fixed-arm robots are now evaluating humanoids for the unstructured tasks that rigid automation cannot handle.

Second, Japan and South Korea's eldercare demand. Japan's demographic reality is stark: over 29% of the population is aged 65 or above, and the ratio is rising. Government procurement programs in both countries explicitly target humanoid-assisted care and rehabilitation as a policy solution to the caregiver shortage — Wave-3 demand arriving earlier than most models projected.

Third, government-led procurement across the region is functioning as a demand anchor. In China alone, municipal funds in Beijing, Shanghai, Shenzhen, and Hubei total ¥26 billion earmarked specifically for humanoid and embodied intelligence programs. South Korea's KIMM declared 2026 the first year of humanoid commercialisation, backed by KRW 220.8 billion. Singapore's EDB committed USD 500 million to position the city-state as ASEAN's humanoid hub.

Three-Wave Deployment Structure

Research and Markets segments the decade ahead into three distinct demand waves. Wave 1 (2025–2030) is industrial and automotive, with price bands of USD 80,000–250,000 per unit. Anchor deployments include BYD-UBTECH (100–200 units), GXO-Agility Robotics (100 contracted), and BMW-Figure (15–30). This wave is already underway.

Wave 2 (2027–2033) targets consumers, developers, and education at USD 5,000–25,000 per unit. Unitree's R1 at USD 5,600 effectively sets the price floor for this segment and signals that the cost curve is compressing faster than most 2023-vintage forecasts assumed.

Wave 3 (2030+) covers medical and elder care — a premium segment gated by safety regulation rather than technology. The long-term total addressable market here is the largest of the three, but deployment timelines hinge on certification frameworks that do not yet exist for autonomous bipedal robots operating near vulnerable populations.

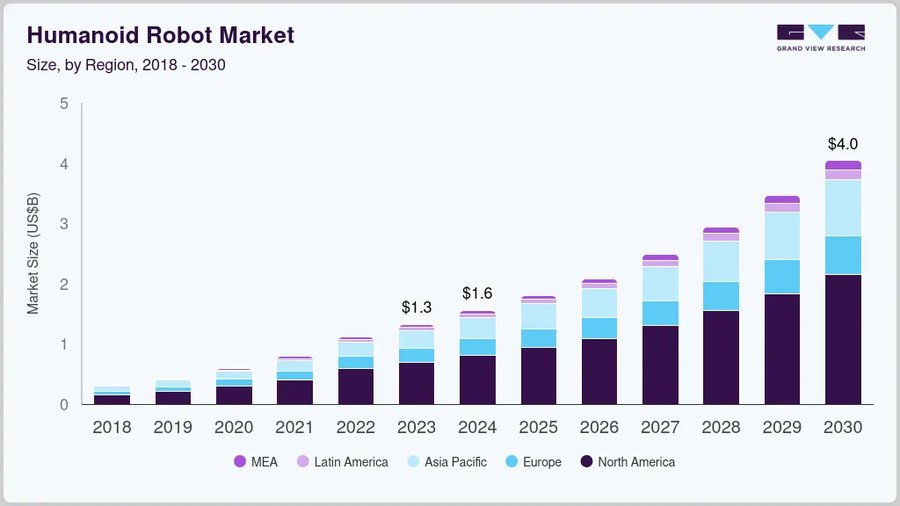

APAC Market Trajectory: $292M to $922M

The Grand View Research trajectory shows consistent compounding: from USD 292 million in 2023 to USD 344M in 2024, USD 405M in 2025, USD 478M in 2026, USD 666M in 2028, and USD 922 million by 2030. These figures represent the baseline scenario — they do not yet incorporate the policy acceleration visible in China's 2025 Government Work Report language or the post-CES 2026 investor enthusiasm.

For industrial buyers evaluating humanoid procurement in the 2026–2027 window, the market structure implies that Wave-1 pricing is near its ceiling. As production volumes scale — AGIBOT targeting 10,000 units in 2026, UBTECH running hundreds of Walker S2 units across multiple automotive plants — per-unit costs will compress. Buyers who pilot now lock in early-mover operational learning before the market commoditises. For investors, the 49% global CAGR is underpinned by real factory deployments, government procurement commitments, and a patent landscape that gives APAC players durable IP moats well into the 2030s.