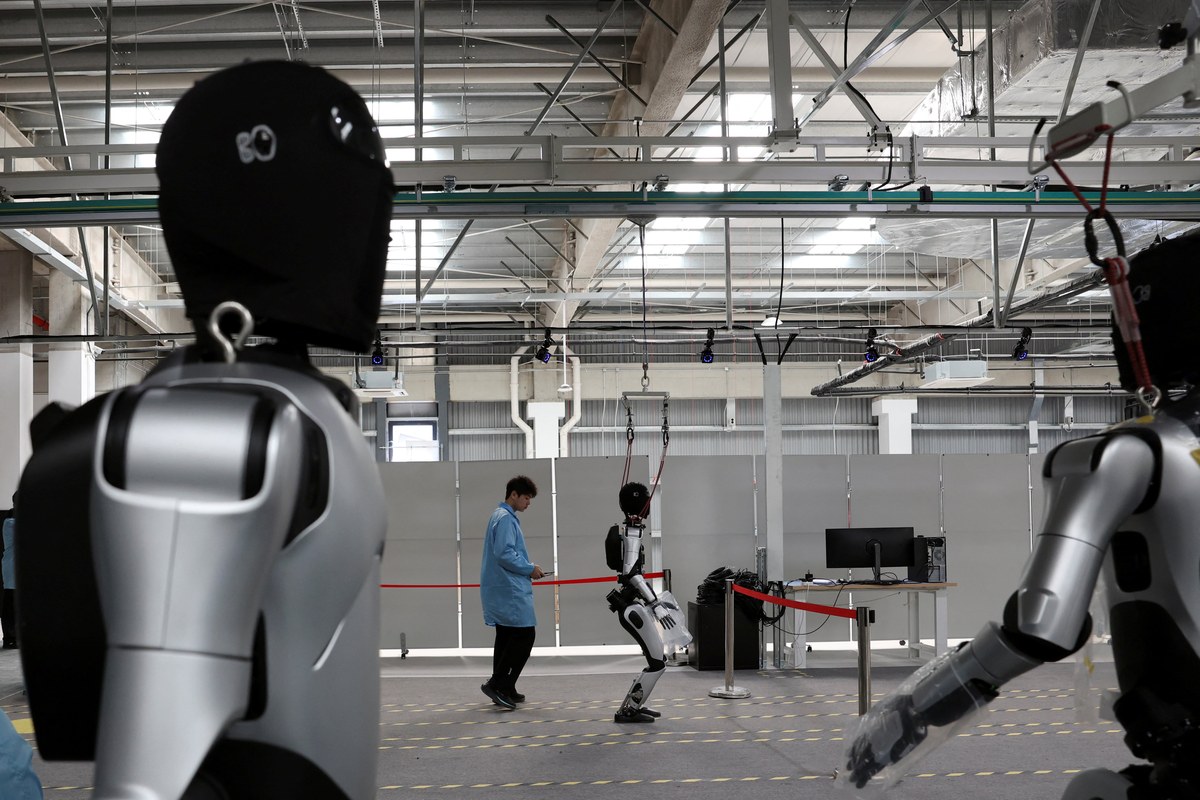

The first quarter of 2026 produced a set of data points across China's humanoid robot industry that, taken together, describe something more significant than incremental progress. They describe a market that is pulling away. China entered the year with approximately 90 percent of global humanoid robot shipments already within its borders — a dominance that is simultaneously a cause and an effect of the supply chain density, manufacturing cost structure, and AI training infrastructure that no other country has yet replicated at anything approaching comparable scale.

The Shipment Scoreboard

AGIBOT, which captured an estimated 38 percent of the global humanoid market in 2025, announced shipment of 10,000 units — a cumulative milestone that establishes it as the highest-volume humanoid manufacturer in the world. Unitree Robotics, having filed for a USD 608 million IPO on the STAR Market, is targeting 20,000 humanoid units in 2026 against 5,500 delivered in 2025 — a trajectory that, if achieved, would represent the largest single-year volume increase any humanoid manufacturer has ever executed. UBTECH is targeting 10,000 Walker S2 units for 2026, a twentyfold increase from its 2025 delivery of roughly 500. These are not the ambitions of three companies that see a crowded field ahead. These are the scaling targets of firms that have already won their segment and are now executing on manufacturing buildout.

GAC Group and the Automotive Entrant

One of the most significant structural signals to emerge from Q1 2026 was the unveiling of GoMate by GAC Group, one of China's largest automotive manufacturers. Humanoid robots designed for automotive assembly and logistics represent the highest-value near-term deployment scenario in the humanoid market — the application that most directly displaces human labor at scale and where per-unit economics are most clearly positive. GAC's entry into humanoid development with a robot purpose-built for its own manufacturing environment is a sign that Chinese industrial conglomerates are beginning to internalize the technology rather than simply purchase it. This vertical integration, if it propagates across other large Chinese manufacturers, would create a demand dynamic that further reinforces China's production volume advantage.

Price Compression as Strategic Weapon

Perhaps the most consequential development of Q1 2026 is the pricing landscape that Chinese manufacturers are establishing. Unitree's R1 at USD 4,900 is a direct assault on the assumption that full humanoid robots require enterprise-level budgets to acquire. The Unitree G1, already available at a competitive price point below USD 20,000, provides the middle tier of a range that has no equivalent in any other national market. This price compression is not achieved through component shortcuts — it is driven by the same supply chain advantages that made China the world's dominant manufacturer of smartphones, EVs, and consumer electronics: vertically integrated supply chains, competition-driven actuator and sensor cost reductions, and manufacturing scale that amortizes tooling costs across volumes no Western competitor can currently match.

Ecosystem Depth: The Marathon as a Proxy

The Beijing E-Town Humanoid Half-Marathon on April 19 provided an unusual but powerful measure of China's humanoid ecosystem depth. One hundred and five teams competed — five times the previous year's count — including five international entrants drawn by the competitive format and the prize structure. The autonomous completion rate of 40 percent, while still a minority, represents a dramatic improvement from 2025 and is a direct output of the training infrastructure, benchmark data, and open competition environment that China has deliberately built around its humanoid industry. When the number of teams capable of fielding a half-marathon robot quintuples in a single year, the talent pipeline, component availability, and development tooling that made it possible cannot be improvised by competitors in 12 months. That is the deepest competitive moat China has built — and it will compound with time.