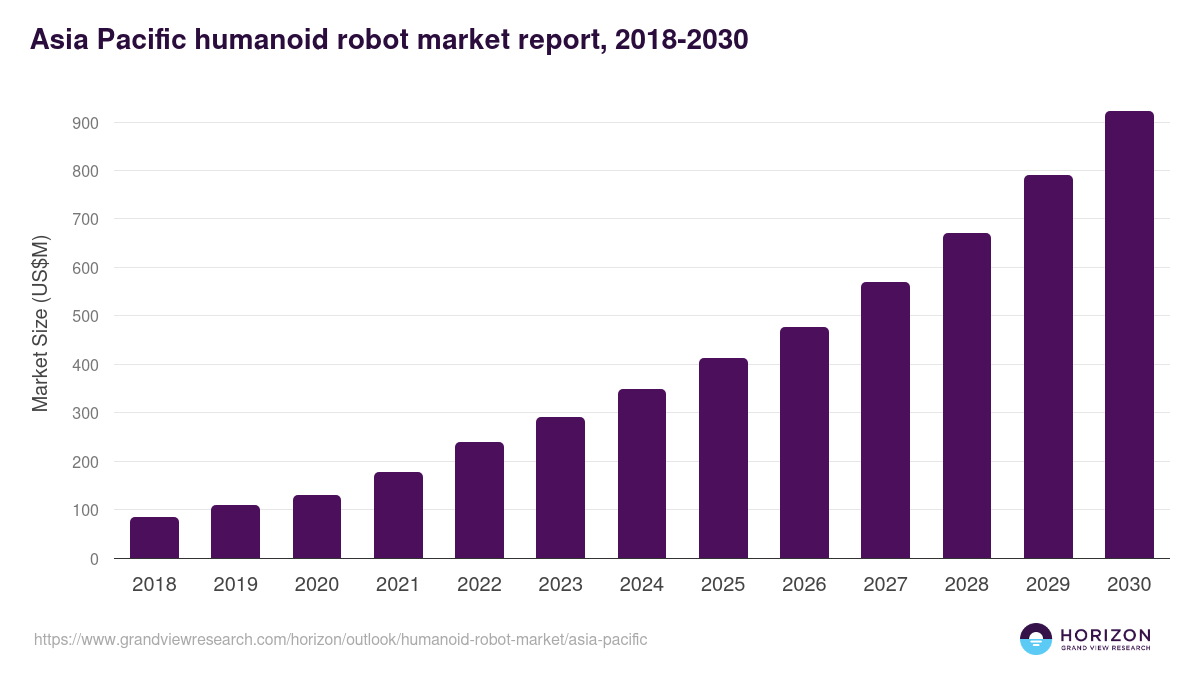

The APAC humanoid robot story in 2025 was defined by breakthroughs: first mass production, first large-scale factory deployment, unprecedented investment flows. The 2026 story will be defined by something harder to capture in a headline — whether the structural foundations of those breakthroughs hold up under commercial pressure. Three signals will determine whether 2026 cements the APAC lead or exposes its first serious cracks.

Signal 1: Can Vendors Break the ¥300,000 / Two-Year Cost Ceiling?

Chinese state procurement is converging on a practical ceiling: a total cost of ownership of ¥300,000 (approximately USD 42,000) over two years, covering hardware, maintenance, energy, and software. Vendors who clear that threshold earn access to 2026 government and SOE tenders — a buyer category that still represents the majority of disclosed humanoid contracts in China.

On the consumer side, Unitree has already cleared this bar: the R1 at USD 5,600 and the G1 at USD 13,500 are priced well below the ¥300,000 ceiling. On the industrial side, UBTECH and AgiBot need to demonstrate that the Walker S2 and A2 series can meet the total-cost-of-ownership requirement through service life, not just list price — which means proving reliability and uptime over 18+ month deployment cycles rather than in controlled demo environments.

Signal 2: Does the Buyer Mix Shift from Education to Industry?

75% of disclosed humanoid orders in H1 2025 came from universities and research institutions, not factories. The BYD-UBTECH deployment and AgiBot's Longcheer facility work are the leading edge of industrial demand, but they represent a small fraction of total units deployed.

The structural question for 2026 is whether the education and government buyer share falls meaningfully as BYD, Geely, and Foxconn ramp Walker S2 production use — or whether industrial deployment proves harder to scale than showcase deployments suggest. Robot reliability in production environments is a fundamentally different problem from robot capability in research settings, and the gap between demonstration throughput and sustained production throughput is where early-stage deployments typically encounter their first challenges.

Signal 3: How Fast Does APAC's Second Tier Emerge?

Japan retains a leadership position in service and elder-care humanoids via SoftBank Robotics and Toyota's Research Institute. With 29%+ of the population aged 65 and above, Japan represents the largest single addressable market for Wave-3 humanoid applications — but Wave-3 is gated on safety regulation that is still being drafted.

South Korea is targeting 30,000 units per year through Hyundai's humanoid program and its Boston Dynamics acquisition. The Korea KIMM declaration that 2026 is the first year of humanoid commercialisation is a procurement signal to Korean industrial groups as much as a policy statement.

Southeast Asia and Taiwan are emerging as component and contract-manufacturing nodes rather than end-market buyers. The APAC actuator and speed reducer sub-market is on a 47.8% CAGR trajectory to USD 345 million by 2032 — driven largely by supply chains being developed in Taiwan and Vietnam to serve Chinese humanoid assemblers.

Four Risks That Could Bend the Curve

Order quality versus order quantity. A 75% education buyer share in 2025 suggests China's disclosed unit volumes may not yet reflect productive commercial demand. If factory adoption stalls at pilot scale, the investment narrative built on shipment milestones will face pressure.

Compute fragmentation. The bifurcation between Chinese silicon (Huawei/Loongson/Biren) and Western silicon (NVIDIA/Qualcomm) creates two parallel software stacks for APAC versus the rest of the world. Vendors attempting to sell into both markets face doubled development costs — a drag that smaller players will struggle to absorb.

Standards drag on Wave-3. Medical and elder-care deployments — the largest long-term TAM — are gated on safety certification frameworks for autonomous bipedal robots that do not yet exist in any major jurisdiction. Even the most optimistic timelines put binding safety standards for elder-care humanoids in the 2028–2030 window.

Capital exuberance and consolidation. 320+ humanoid companies in China cannot all reach commercial scale. The consolidation pressure expected from H2 2026 onward will create winners and casualties — and the transition period will likely produce pricing uncertainty, customer hesitation, and supply chain disruption as smaller vendors exit and customers requalify alternative suppliers.